What Is Fintech Regulation and Why It Matters

- NUR Legal

- Dec 12, 2025

- 6 min read

Most british financial technology startups underestimate just how quickly regulations evolve in this competitive market. With over 60 percent of FinTech leaders naming compliance as their biggest hurdle, the impact of changing legislation can never be ignored. Understanding the shifting nature of FinTech regulation empowers innovators and businesses to adapt fast, avoid costly mistakes, and stay ahead in a rapidly changing financial landscape.

Table of Contents

Key Takeaways

Point | Details |

FinTech Regulation Complexity | The regulatory landscape for financial technology is evolving, requiring businesses to adapt to protect consumers and maintain stability. |

Regulatory Framework Types | Diverse regulatory approaches are employed globally, including prescriptive, risk-based, principles-based regulations, and regulatory sandboxes. |

Licensing and Compliance | Financial technology businesses must navigate stringent licensing and registration processes, ensuring compliance to avoid penalties. |

Risk Management Importance | Companies must implement robust risk management strategies to address systemic vulnerabilities inherent in technological advancements. |

Fintech Regulation Defined and Debunked

Financial technology (FinTech) represents a rapidly evolving landscape where technological innovation intersects with traditional financial services. At its core, financial technology regulation addresses the complex legal frameworks governing digital financial platforms, payment systems, blockchain technologies, and emerging financial service models.

The regulatory environment for FinTech has become increasingly sophisticated, reflecting the sector’s dynamic nature. Financial regulatory bodies are continuously adapting their approaches to manage the opportunities and challenges presented by technological disruption. These regulations aim to protect consumers, maintain financial stability, prevent fraudulent activities, and ensure transparent operational standards across digital financial ecosystems.

Key aspects of FinTech regulation typically encompass several critical domains:

Licensing and Registration: Establishing clear requirements for digital financial service providers

Consumer Protection: Safeguarding user data and financial interests

Anti-Money Laundering (AML) Compliance: Preventing financial crimes in digital transactions

Data Privacy: Implementing robust security protocols for sensitive financial information

Academic research on financial technology law suggests that regulatory frameworks must balance innovation with risk management. This means creating flexible guidelines that encourage technological advancement while maintaining sufficient oversight to protect market participants. The ultimate goal is not to stifle innovation but to create a secure, trustworthy environment where digital financial services can thrive responsibly.

Understanding FinTech regulation requires recognising it as a dynamic, evolving field. Regulatory approaches will continue to transform as technologies advance, making ongoing education and adaptability crucial for businesses operating in this space.

Types of Fintech Regulatory Frameworks

Financial technology regulation encompasses diverse approaches designed to address the complex challenges posed by technological innovation in financial services. Regulatory frameworks vary significantly across jurisdictions, reflecting different national priorities, risk tolerances, and technological readiness.

Evolutionary game models demonstrate the intricate interactions between regulators and financial institutions, revealing multiple strategic regulatory approaches. These frameworks typically fall into several distinct categories:

Prescriptive Regulation: Strict, rule-based frameworks with detailed compliance requirements

Risk-Based Regulation: Adaptive approaches focusing on potential systemic risks

Principles-Based Regulation: Flexible guidelines emphasising overall conduct and outcomes

Regulatory Sandboxes: Controlled environments for testing innovative financial technologies

Comparative research on regulatory sandboxes highlights how different jurisdictions create unique approaches to managing financial innovation. Some countries adopt highly permissive models that encourage technological experimentation, while others maintain more conservative oversight mechanisms.

The primary objectives of these regulatory frameworks remain consistent: protecting consumer interests, maintaining financial system stability, preventing fraudulent activities, and fostering responsible technological innovation. As financial technologies continue to evolve rapidly, regulatory approaches must remain adaptive, balancing technological potential with robust risk management strategies.

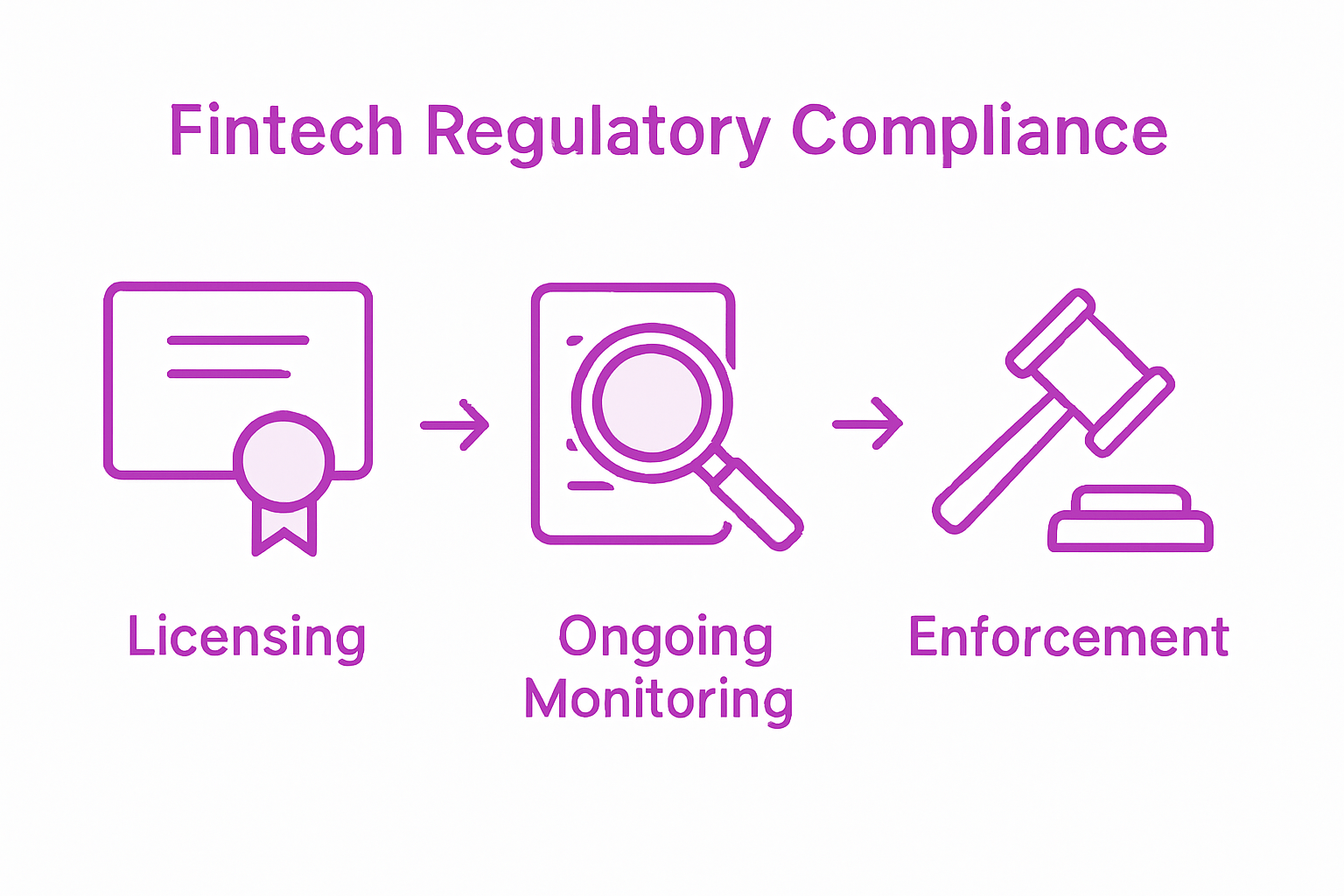

Licensing, Registration, and Key Obligations

Financial technology businesses operate within a rigorous regulatory landscape that demands comprehensive licensing and registration processes. These mandatory requirements serve as critical gatekeepers, ensuring only qualified and compliant organisations can offer financial services to consumers and businesses.

Securities regulation frameworks establish detailed requirements for financial service providers, encompassing multiple layers of operational scrutiny. Financial technology companies must navigate complex registration protocols that typically involve:

Detailed corporate documentation submission

Comprehensive background checks on key personnel

Proof of sufficient financial capital

Robust risk management infrastructure

Demonstrable compliance capabilities

Regulatory organisations like FINRA monitor industry compliance through systematic oversight mechanisms. These mechanisms assess whether financial technology entities maintain appropriate standards of professional conduct, technological security, and consumer protection.

Key obligations extend beyond initial registration, requiring ongoing compliance and periodic reporting. Companies must continuously demonstrate their ability to manage financial risks, protect customer data, prevent money laundering, and maintain transparent operational practices. Failure to meet these stringent requirements can result in significant penalties, including licence suspension or revocation, underscoring the critical importance of thorough and consistent regulatory adherence in the financial technology sector.

Compliance, Reporting, and Enforcement Issues

Financial technology organisations face increasingly complex compliance and reporting landscapes that demand meticulous attention to regulatory requirements. These frameworks are designed to ensure transparency, protect consumer interests, and maintain the integrity of financial systems.

Securities regulators enforce comprehensive reporting mechanisms that require financial technology companies to submit detailed documentation demonstrating their operational compliance. These reporting obligations typically encompass:

Periodic financial statements

Transaction monitoring records

Risk management assessments

Compliance programme documentation

Anti-money laundering verification reports

Regulatory oversight involves systematic examination processes that scrutinise organisational practices, technological infrastructure, and adherence to established guidelines. Enforcement actions can range from formal warnings to significant financial penalties and potential licence revocations.

The consequences of non-compliance extend beyond immediate financial penalties. Organisations may experience reputational damage, reduced investor confidence, and potential legal challenges. Successful financial technology businesses must therefore develop robust internal compliance frameworks that proactively anticipate and address regulatory requirements, transforming compliance from a mere administrative burden into a strategic operational advantage.

Risks, Liabilities, and Common Pitfalls

Financial technology organisations confront a complex landscape of systemic and operational risks that demand sophisticated risk management strategies. The dynamic nature of technological innovation creates multiple potential vulnerabilities that can compromise organisational stability and regulatory compliance.

Systemic risk analysis reveals interconnected financial system vulnerabilities that financial technology companies must carefully navigate. These risks typically manifest across several critical domains:

Technological infrastructure fragility

Cybersecurity exposure

Data privacy breaches

Regulatory non-compliance

Operational resilience challenges

The most prevalent pitfalls for financial technology businesses often stem from inadequate risk assessment and management protocols. Companies frequently underestimate the complexity of maintaining robust technological and regulatory safeguards, leading to potential financial and reputational consequences.

Effective risk mitigation requires a proactive, comprehensive approach that integrates technological resilience with rigorous compliance frameworks. Organisations must develop adaptive risk management strategies that anticipate potential vulnerabilities, implement robust monitoring systems, and maintain the flexibility to respond swiftly to emerging technological and regulatory challenges.

Navigate FinTech Regulation with Expert Legal Support

Understanding the complex regulatory environment in financial technology is essential for any business aiming to succeed in this fast-evolving sector. The article highlights critical challenges such as licensing, compliance, consumer protection, and risk management. Without the right legal guidance, navigating these intricate frameworks can lead to costly pitfalls and stalled growth.

At NUR Legal, we specialise in helping startups and established businesses secure the appropriate licences and maintain full regulatory compliance across jurisdictions. Our services include crypto and gaming licences, company formation, and tailored legal opinions designed to address the unique risks of high-risk, regulated industries. Take control of your FinTech venture by partnering with experts who understand the fine balance between innovation and regulation.

Ready to build a legally compliant and resilient operation in financial technology? Explore our comprehensive offerings at NUR Legal and discover how our trusted licensing solutions and legal consultancy can safeguard your business. Visit our main site now to start your journey towards regulatory success and operational confidence.

Frequently Asked Questions

What is fintech regulation?

Fintech regulation refers to the legal frameworks governing digital financial platforms and services. These regulations aim to protect consumers, ensure financial stability, and prevent fraud in the rapidly evolving financial technology sector.

Why is fintech regulation important?

Fintech regulation is crucial because it helps safeguard consumer interests, maintains the integrity of financial systems, and fosters innovation. It creates a secure environment for digital financial services while mitigating risks associated with technological advancement.

What are the key components of fintech regulation?

Key components of fintech regulation include licensing and registration processes, consumer protection measures, anti-money laundering compliance, and data privacy protocols. These elements ensure that financial technology companies operate transparently and responsibly.

How do regulatory frameworks for fintech differ across jurisdictions?

Regulatory frameworks for fintech vary significantly across jurisdictions, incorporating different priorities and risk tolerances. Some approaches may be prescriptive with strict compliance requirements, while others may adopt more flexible, principles-based guidelines or create regulatory sandboxes for experimental innovation.

Recommended

Comments