Step-by-Step Guide to Company Formation Worldwide

- NUR Legal

- Jan 23

- 18 min read

Building a fintech or crypto startup in Europe or Southeast Asia often means facing layers of regulatory challenges before you can even get started. Picking the right jurisdiction and legal structure affects your business model, tax exposure, and how quickly you can operate. With every country setting unique standards, a smart approach recognises that evidence-based, inclusive rulemaking and early expert consultation can avoid wasted time and costly mistakes. Here you gain the insights needed to navigate formation, secure licensing, and maintain compliance in high-risk sectors.

Table of Contents

Quick Summary

Key Insight | Explanation |

1. Assess Regulatory Requirements Early | Understanding local regulatory requirements helps identify the viability and costs of your business model. |

2. Choose the Right Jurisdiction | Select a jurisdiction with appropriate regulatory support and cost-effectiveness for your specific business type. |

3. Prepare Comprehensive Documentation | Meticulously assemble required documentation to ensure swift registration and licensing approval from regulators. |

4. Maintain Ongoing Compliance | Establish a compliance calendar and monitor regulatory changes to avoid penalties or operational disruptions. |

5. Engage Professional Advisors | Consult with local legal and tax experts early to uncover potential challenges before committing to any jurisdiction. |

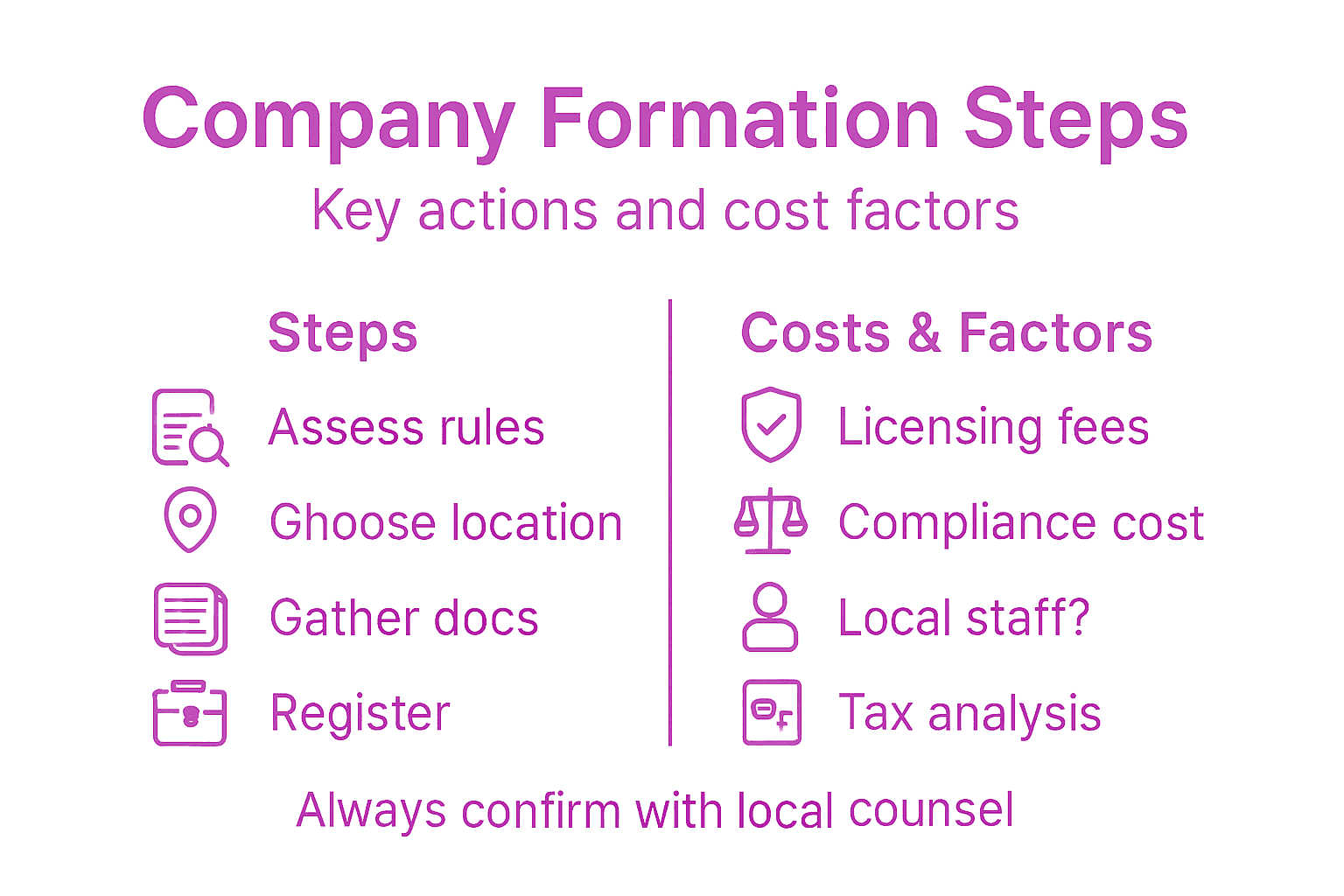

Step 1: Assess regulatory requirements and feasibility

Before you invest time and resources into launching your company, you need to understand what regulators actually require in your target jurisdiction. This step determines whether your business model is viable, what costs you’ll face, and how long the entire process will take. Getting this wrong at the beginning means wasting months and significant capital pursuing an impossible path.

Start by identifying which regulatory bodies govern your industry in your chosen jurisdiction. For fintech and crypto ventures, this typically involves multiple authorities: financial regulators, tax authorities, data protection bodies, and sometimes gambling commissions or anti-money laundering specialists. Each has different priorities and timelines. In European jurisdictions, the Financial Conduct Authority or equivalent national bodies set the rules. In Southeast Asia, you might deal with the Monetary Authority of Singapore, Thailand’s Securities and Exchange Commission, or Indonesia’s Financial Services Authority. Document exactly which agencies matter for your specific business model.

Next, research the actual licensing pathways available to you. Not every jurisdiction offers every licence type. Some countries provide a streamlined fintech sandbox licence for startups, whilst others require full banking or securities licenses from day one. The Curaçao jurisdiction, for instance, offers comprehensive gaming and digital asset licensing at a fraction of the cost and timeline of European alternatives. Seychelles and Georgia have become popular for crypto operations due to their tailored regulatory frameworks. Your task is to find where your specific business type is not just allowed, but actively supported with reasonable timelines and costs.

Conduct preliminary consultations with local legal counsel or compliance specialists before making any commitments. They can tell you whether your business model requires advance approval, what documentation you’ll need to gather, and what the realistic timeline actually is. Evidence based regulatory assessment combined with stakeholder consultation processes creates clearer pathways for compliance from the start. You should also research whether your jurisdiction participates in international standards alignment programmes, as this affects how easily you can operate across borders later.

Examine the financial feasibility alongside regulatory requirements. Calculate the licensing fees, ongoing compliance costs, reporting requirements, and staff expenses needed to maintain your licence. Some jurisdictions charge annual licensing fees equivalent to thousands of pounds; others charge tens of thousands. Build a spreadsheet comparing at least three jurisdictions side by side. Factor in the cost of professional advisors, bank accounts, compliance software, and legal reviews. Many fintech founders discover halfway through that their chosen jurisdiction’s costs make their business model unworkable.

Review the specific operational requirements your chosen jurisdiction imposes. Does the regulator require you to hold a minimum amount of capital? Do they mandate specific compliance officers or directors? Must your servers be located within the country or can they be hosted internationally? Will you need separate entities for different product lines or can you operate everything under one licence? These operational details significantly affect your formation strategy and ongoing costs. Understanding these requirements upfront means you won’t face unexpected compliance demands after you’ve already launched.

Assess the political and regulatory stability of your target jurisdiction. A cheap licence means little if the regulatory environment shifts dramatically in two years or if the jurisdiction faces international sanctions or loses banking relationships. Research whether the country is engaged in international cooperation for effective regulation and maintains good standing with international bodies. Check whether other established companies in your industry maintain licences there, as this signals stability.

Here is a comparison of regulatory environments for popular fintech and crypto jurisdictions:

Jurisdiction | Regulatory Approach | Typical Licensing Costs | Banking Environment |

United Kingdom | Established, stringent oversight | High (£10,000+ p.a.) | Strong banking sector |

Curaçao | Streamlined, crypto-friendly | Moderate (£5,000+ p.a.) | Moderate, niche providers |

Singapore | Innovative, rigorous compliance | High (£15,000+ p.a.) | Highly accessible, global |

Georgia | Tailored, pro-digital assets | Low (£2,000+ p.a.) | Limited, growing options |

Seychelles | Specialised, flexible for crypto | Low (£2,500+ p.a.) | Challenging, some access |

Once you have clear information about regulatory requirements, feasibility, and costs, document your findings in a decision memo. This becomes your baseline for all subsequent formation steps and helps you justify your jurisdiction choice to investors, board members, or co-founders. You now have the intelligence needed to move forward confidently rather than discovering critical obstacles later.

Pro tip: Request a preliminary regulatory assessment from local counsel before committing to any jurisdiction; this typically costs between £500 and £2,000 and saves you from pursuing jurisdictions where your business model simply won’t be approved.

Step 2: Select optimal jurisdiction and legal structure

With regulatory requirements mapped out, you now need to decide where to formally incorporate and what legal entity type best serves your business. This decision shapes your tax obligations, operational flexibility, personal liability exposure, and how easily you can scale internationally. Getting this right saves you thousands in unnecessary taxes and prevents structural problems that become expensive to fix later.

Your jurisdiction choice and legal entity type are interconnected decisions. A private limited company in the United Kingdom operates under completely different rules than a limited liability company in Singapore or a digital asset company in Curaçao. Start by matching your refined business model against the jurisdictions you identified as feasible in step one. For fintech and crypto startups, this often means choosing between established financial centres like the UK, Singapore, and Malta; specialist crypto jurisdictions like Curaçao, Georgia, and Seychelles; or offshore structures in places like the British Virgin Islands or Mauritius. Understanding how to optimise legal structures while managing tax liabilities requires balancing immediate compliance costs against long-term operational efficiency.

Consider the legal entity types available in each jurisdiction. Most fintech and crypto companies operate as either a private limited company (closest to a private corporation), a limited liability company (LLC), or a special purpose digital asset company. Private limited companies offer personal liability protection and are recognised globally, making them ideal for regulated financial services. LLCs provide operational flexibility and pass-through taxation in some jurisdictions, which appeals to many startups. Digital asset companies, now available in Georgia, Curaçao, and Seychelles, are specifically designed for crypto and blockchain ventures with tailored compliance requirements. Each structure has different capital requirements, director obligations, reporting standards, and compliance costs. A UK private limited company requires proper company secretarial services and statutory filings; a Curaçao digital asset company may have simpler ongoing requirements but less international recognition.

Tax implications deserve serious analysis at this stage. Different jurisdictions offer different tax treatments for the same business activity. A fintech company in Singapore might pay corporate income tax on profits but benefit from extensive tax treaties; the same company in Mauritius might enjoy substantially lower tax rates with different treaty networks; whilst a Curaçao entity might operate under a different tax regime entirely. You must understand not just where you incorporate, but how that choice affects taxes in jurisdictions where you actually earn revenue and where your investors are located. Calculate your projected tax liability under each scenario before deciding. Many founders prioritise cheap licensing costs without realising they’ll pay significantly higher taxes over five years.

Evaluate operational requirements for each entity type and jurisdiction combination. Will you need local staff or can you operate with overseas directors and a registered agent? Can meetings happen virtually or must you conduct them locally? Where must records be kept? What are the annual filing deadlines and penalties for missing them? Some jurisdictions require substantial local infrastructure; others are entirely virtual. For high-risk industries like fintech and crypto, regulatory scrutiny around beneficial ownership and operational transparency has increased substantially. You want a structure that demonstrates genuine operations, not one that looks like a shell company to regulators and banking partners.

Banking relationships should influence your choice more than many founders realise. A company registered in a well-regulated jurisdiction with strong compliance frameworks will find banking partners relatively easily. Entities from jurisdictions with reputational concerns face banking difficulties that can cripple your operations. Your bank needs to feel comfortable with your regulatory status and jurisdiction choice. Speak with potential banking partners early to understand their appetite for entities from your shortlisted jurisdictions. This often eliminates options that looked good on paper but prove impossible operationally.

Draft a comparison matrix covering at least your top three jurisdiction and entity type combinations. Include incorporation costs, annual compliance costs, tax rates, required capital, director requirements, banking accessibility, regulatory recognition, and operational flexibility. Assign weightings to factors that matter most for your specific business. A consumer fintech app might prioritise EU recognition and regulatory credibility; a crypto trading platform might prioritise lower tax rates and specialist crypto licensing; a payment processor might prioritise banking relationships and compliance infrastructure. Your matrix becomes the evidence for your final selection.

Professional insight: Consult with a tax advisor and compliance specialist in your top two jurisdictions before incorporating; spending £1,500 to £3,000 on preliminary advice often reveals tax inefficiencies or banking obstacles that would cost exponentially more to fix after you’ve already registered your company.

Step 3: Prepare documentation and compliance materials

You now move into the practical work of assembling everything regulators and company registration authorities need to approve your business. This step determines whether your application gets approved quickly or gets rejected and sent back for corrections. The quality of your documentation directly affects your timeline and the credibility you establish with regulatory bodies from day one.

Start by obtaining a comprehensive checklist specific to your chosen jurisdiction and entity type. This checklist should come from your legal advisor or the company registration authority itself. For a UK private limited company, you will need articles of association, director identification, registered office confirmation, and shareholder information. For a Curaçao digital asset company, you might need beneficial ownership declarations, compliance officer details, and anti-money laundering policy documentation. For a Singapore fintech entity, you will need director declarations, compliance frameworks, and potentially proof of office premises. The checklist you create becomes your roadmap. Tick off each item as you complete it rather than preparing documents randomly and hoping you have everything.

Prepare your corporate governance documentation meticulously. Articles of association, bylaws, or company constitutions set out how your company will operate internally. These documents must be consistent with your actual business operations and cannot contradict regulatory requirements. Directors and shareholders need clear written agreements defining their roles, decision-making authority, and responsibilities. For high-risk industries like fintech and crypto, governance documentation often receives detailed regulatory scrutiny. Auditors and compliance teams will review these documents to understand your decision-making processes and verify that decisions follow proper procedures. Draft these carefully or have experienced legal counsel prepare them rather than using generic templates that may not align with your specific structure.

Gather and prepare identification documentation for all directors, shareholders, and beneficial owners. Regulators want to verify that real people with legitimate backgrounds control your company. You will typically need certified copies of passports or identity documents, proof of address (utility bills no older than three months), and sometimes criminal background checks. For companies with complex ownership structures, prepare detailed beneficial ownership declarations showing the chain of ownership and control. Some jurisdictions require source of funds declarations proving that shareholder capital comes from legitimate sources. This documentation seems straightforward but takes time to collect from international shareholders. Start this process early because tracking down certified documents from people across multiple countries can introduce unexpected delays.

Develop your anti-money laundering and compliance policies aligned with regulatory expectations. Regulators scrutinise how seriously you take financial crime prevention. Your policies must address customer due diligence, transaction monitoring, suspicious activity reporting, and staff training. The specific requirements vary dramatically by jurisdiction and by whether you are a payment processor, exchange, lending platform, or trading service. Preparing detailed documentation and compliance materials aligned with regulatory frameworks ensures you meet approval standards on your first submission rather than through multiple revision rounds. Your compliance policies should be practical and actually implementable by your team rather than theoretical exercises that look impressive on paper but cannot be executed in reality. If you are outsourcing compliance functions, document the service level agreements and vendor qualifications clearly.

Prepare financial documentation demonstrating your company’s financial stability and source of capital. This might include bank statements showing initial capital deposits, accountant certifications of financial position, or evidence of funding from legitimate sources. Regulators want confidence that your company can sustain operations and meet financial obligations to customers. If you have received investment funding, prepare documentation of shareholder agreements and investment terms. If you are bootstrapping, demonstrate that you have sufficient personal funds available. For payment processors and lending platforms especially, regulators want detailed financial projections and stress test scenarios showing how your company survives market downturns.

Compile regulatory filings and supporting documents required by your chosen jurisdiction. This includes articles of association, director declarations, compliance officer appointments, compliance policies, anti-money laundering procedures, and sometimes statutory declarations under oath. Some jurisdictions require you to file these documents with the registration authority; others require you to hold them ready for inspection. Create both a master file with original documents and a second file with copies organised exactly as regulators expect them. Submit through official channels rather than informal methods. Many rejections result not from missing information but from documents submitted in the wrong format or through incorrect channels.

Obtain professional certifications if required by your jurisdiction. Some countries require directors to complete compliance training or certifications. Others require compliance officers to hold specific qualifications. Georgia and Seychelles, for example, have specific requirements for who can serve as beneficial owner or compliance officer. Identify these requirements early and plan time for certifications or recruitment of appropriately qualified staff. Do not assume you can obtain a waiver or exception just because obtaining the qualification seems difficult.

Professional advice: Prepare 20 percent more documentation than regulators technically require, organising everything clearly with index pages and cross references; this demonstrates professionalism and dramatically increases approval likelihood on your first submission rather than triggering requests for additional information that extend your timeline by weeks or months.

The following table summarises core documentation needed for fintech and crypto company formation:

Document Type | Purpose | Common Issues |

Articles of Association | Define company operations | Inconsistency with law |

Identity Verification | Confirm director/shareholder details | Outdated documents |

Compliance Policies | Demonstrate AML and risk controls | Unpractical procedures |

Financial Statements | Show financial strength and funding | Lack of detail |

Beneficial Ownership Declarations | Reveal control and transparency | Complex structures |

Step 4: Register company and secure licences

You have assessed feasibility, chosen your jurisdiction, and prepared your documentation. Now comes the point where your company actually becomes legal and licensed to operate. This step transforms your plans into a registered entity with regulatory approval. The registration and licensing process varies dramatically by jurisdiction, but understanding the general sequence and common pitfalls helps you navigate it efficiently.

Begin by submitting your company registration application to the appropriate authority in your chosen jurisdiction. For a UK private limited company, you file with Companies House. For a Curaçao digital asset company, you register with the Curaçao Financial Services Commission. For Singapore, you register with the Accounting and Corporate Regulatory Authority. Each authority has specific submission procedures, fees, and timelines. Some accept only electronic submissions; others still require physical documents. Check the official government website rather than relying on third party guidance that may be outdated. Pay particular attention to the exact document format required, whether documents need certification or notarisation, and whether you need to submit originals or certified copies. The procedural steps for company registration internationally require conforming to each jurisdiction’s specific legal requirements and timelines to ensure successful approval without delays caused by administrative errors.

Once your application is submitted, the registration authority reviews your documentation against their requirements. This review period typically takes between two weeks and three months depending on the jurisdiction. Some authorities conduct thorough background checks on directors and beneficial owners; others perform minimal verification. Be responsive during this period. If the authority requests clarifications or additional documents, respond promptly and thoroughly. Delayed responses extend your timeline significantly. Some jurisdictions assign you a company registration number during application; others issue it only after full approval. Clarify with the registration authority what stage you have reached and what remains outstanding. Do not assume approval simply because you have not heard negative feedback.

After company registration approval, you move into the licensing phase if your business requires specific regulatory licences beyond basic company registration. Most fintech and crypto operations do require additional licences. These operate on a separate timeline from company registration. You may need to hold a registered company before you can apply for a financial services licence, or you may apply simultaneously. Curaçao, Georgia, and Seychelles offer digital asset licences with relatively streamlined processes; Europe, Singapore, and other major financial centres have more intensive licensing requirements involving background checks, capital requirements verification, and compliance framework assessments. The licensing application process is typically where high-risk industry operators spend most of their time and resources. Expect the licensing authority to request extensive documentation, conduct site visits, interview management, and demand explanations of your compliance procedures.

Understand that regulatory approval processes including registration with relevant authorities and obtaining necessary licences often require multiple clearances and documentation verifications, with strategic registration sequences facilitating faster market entry. Some jurisdictions allow provisional operation whilst your licence application is under review; others prohibit any operations until full licence approval. Know which applies to your situation before you start customer acquisition or fund transfers. Operating without proper licensing exposes you to regulatory enforcement, substantial fines, and personal liability for directors. The risk is not worth attempting to operate in the gap between registration and licensing.

Prepare for the possibility of a conditional licence or licence requiring specific undertakings. Some regulators approve your licence but attach conditions such as mandatory compliance officer appointments, specific audit requirements, or restrictions on certain customer types. Review the conditions carefully and confirm you can meet them before accepting the licence. Refusing a conditional licence at this stage is far easier than attempting to modify licence conditions after operations begin. If conditions are unacceptable, consult with your legal advisor about whether negotiation is possible or whether you should reconsider this jurisdiction.

After receiving your full registration certificate and operating licence, obtain any additional authorisations required before you can legally commence business. This might include banking authorisation from your bank, API credentials from payment processors, or cryptocurrency exchange listings. Confirm with each service provider exactly what documentation they require before they will activate your account. Some require certified copies of your licence; others conduct their own background checks despite your regulatory approval.

Throughout this process, maintain detailed records of every submission, response, and communication with registration and licensing authorities. Create a master timeline documenting when you submitted each document, when you received acknowledgement, and when you received decisions. This documentation proves compliance if regulators later question your registration process and helps you track where you stand in a multi-stage approval process.

Professional tip: Appoint a dedicated compliance contact at the registration and licensing authority early in your process; building a working relationship with the actual person reviewing your application often accelerates approvals and helps clarify ambiguous requirements before they become reasons for rejection.

Step 5: Verify registration and maintain ongoing compliance

Your company is now registered and licensed. Many founders believe this marks the end of the process, but registration is actually just the beginning. Maintaining your registration in good standing and staying compliant with evolving regulations requires consistent effort, structured processes, and ongoing attention. This final step determines whether your company remains operational or faces suspension, penalties, or enforcement action down the line.

First, verify that your registration is actually complete and reflects what you submitted. Request official documentation from the registration authority confirming your company exists in their systems with the correct details. Check that your company name, registered office address, directors, and beneficial owners all match your records. Discrepancies at this stage are far easier to fix than discovering problems months later. Request certified copies of your registration certificate and any licence documentation. These become your proof of legal status when opening bank accounts, entering contracts, or dealing with regulators. Store originals in secure locations and maintain digital backups in cloud storage accessible to authorised personnel only.

Establish a compliance calendar covering all mandatory deadlines for your jurisdiction and industry. Most jurisdictions require annual financial accounts filing, director and shareholder confirmations, beneficial ownership updates, and annual compliance certifications. The UK requires Companies House filings annually; Curaçao requires annual regulatory compliance reports; Singapore requires multiple filings depending on your business type. Missing even one deadline can result in penalties, suspension of your licence, or removal from the registry. Create a master spreadsheet listing every deadline, what document is required, who is responsible for preparing it, and when you must submit it. Set reminders 60 days before each deadline to ensure nothing gets forgotten.

Implement ongoing regulatory monitoring to track changes that affect your business. Regulations change frequently, particularly in fintech and crypto where jurisdictions continually refine their approaches. Subscribe to regulatory update newsletters from your jurisdiction’s financial authority. Join industry associations that provide regulatory alerts. Maintain regular contact with your compliance advisors or legal counsel to stay informed of material changes. Regulations that change may require updates to your compliance policies, staff training, operational procedures, or even your business model. Continual regulatory monitoring and adaptation to changing regulations ensures sustained lawful operations and good standing globally. Failing to adapt to regulatory changes leaves you vulnerable to enforcement action based on requirements you did not know existed.

Maintain meticulous records of all compliance activities and regulatory interactions. Document when you completed staff training, when you conducted compliance reviews, when you filed reports, and how you responded to regulatory requests. If regulators ever question your compliance later, these records demonstrate that you took your obligations seriously. Poor record keeping looks like negligence even if you actually complied. Keep originals and backups of all filed documents, confirmations of receipt, and correspondence with authorities. Some jurisdictions require records to be kept for seven years or longer. Budget storage space and budget for document management systems that make retrieval straightforward.

Continue updating your beneficial ownership declarations, director information, and compliance officer details whenever changes occur. Many enforcement actions against fintech and crypto companies stem from outdated beneficial ownership information or unregistered management changes. If a director resigns and you forget to notify the authority, you are technically in violation even if you genuinely forgot. Implement a process where any management or ownership changes trigger immediate notifications to relevant authorities. Make this someone’s explicit responsibility rather than assuming it will happen organically.

Conduct regular internal compliance reviews examining whether your actual operations align with your licence conditions and compliance commitments. Many companies create impressive compliance policies at formation but then do not actually follow them. Regulators discovering this disconnect during audits or investigations leads to enforcement action and potential licence suspension. Annually, review your compliance policies, confirm they are being followed in practice, and update them to reflect actual operations. Document the review process and maintain records showing senior management involvement in compliance oversight.

Prepare for regulatory examinations and audits. Most financial regulators conduct periodic examinations of licensed companies. When the regulator requests information or announces an examination, treat this as a priority. Respond completely and honestly. Provide requested documents promptly. Prepare management and staff for interviews. Regulatory examinations are normal business events for regulated companies, not signs that something is wrong. However, poor preparation or incomplete responses create suspicion and often lead to enforcement recommendations.

Maintain sufficient capital and financial resources to meet ongoing regulatory requirements. Some licences require you to maintain minimum capital thresholds. Others require you to hold funds belonging to customers separately in segregated accounts. Ensure your financial position always meets these requirements. Falling below required capital levels is grounds for licence suspension regardless of your other compliance efforts.

Professional guidance: Engage a local compliance officer or outsourced compliance service provider in your jurisdiction to monitor regulatory changes and manage compliance calendars, particularly if you operate in multiple jurisdictions; this costs between £2,000 and £10,000 annually but prevents costly enforcement actions and licence suspensions resulting from missed deadlines or regulatory changes.

Simplify Your Global Company Formation with Expert Legal Support

Navigating complex regulatory frameworks and diverse licensing requirements can be overwhelming when forming a company worldwide, especially in high-risk sectors like fintech and crypto. If you are facing challenges such as understanding jurisdictional feasibility, managing compliance documentation, or securing licences efficiently, you are not alone. The detailed step-by-step guide highlights how crucial it is to balance regulatory demands with operational agility and cost effectiveness.

At NUR Legal, we specialise in precisely these problem areas. From assisting with company formation across key jurisdictions including Curaçao, Georgia, and Seychelles to providing comprehensive licensing services and compliance support, we help you avoid costly mistakes and delays. Our strong relationships with regulators and deep knowledge of licence structures ensure your application stands out with credible documentation and proper legal frameworks.

Take the guesswork out of your next steps. Whether you need a fast and affordable gaming licence or a robust crypto licence tailored to your business, trust our team to streamline your formation and licensing journey. Visit NUR Legal now to explore our global company formation solutions and secure your place in regulated markets with confidence. Begin your compliant and sustainable business venture today by clicking here to discover how we can assist you at NUR Legal. Learn more about our trusted licensing offerings in Curaçao full Gaming Licensing or Crypto Licences in Georgia and Seychelles to take immediate action.

Frequently Asked Questions

What are the initial steps to assess regulatory requirements for company formation?

To assess regulatory requirements, start by identifying the governing authorities in your target jurisdiction. Next, research the specific licences needed for your business model and consult with local legal experts to ensure all documentation aligns with regulatory expectations.

How do I choose the optimal jurisdiction for my company?

To choose the optimal jurisdiction, compare multiple locations based on their regulatory frameworks, licensing costs, and operational requirements. Create a comparison matrix that highlights key factors such as compliance costs and banking accessibility, and select the one that aligns best with your business needs.

What documentation is required for company registration?

The necessary documentation typically includes articles of association, identification for directors and shareholders, and compliance policies. Compile a comprehensive checklist based on your jurisdiction to ensure you prepare all required documents accurately.

How long does the company registration process take?

The company registration process can vary widely, often taking anywhere from two weeks to three months depending on the jurisdiction’s specific requirements. Submit all necessary documentation promptly to help expedite approval and avoid delays.

What ongoing compliance tasks must I manage after registration?

After registration, you must keep track of compliance tasks such as annual financial filings, updating ownership information, and maintaining records of compliance activities. Establish a compliance calendar to help you meet all deadlines and regularly review your processes to ensure they align with regulatory standards.

How can I ensure my business remains compliant with changing regulations?

To remain compliant, engage in continuous regulatory monitoring to track changes that affect your business operations. Subscribe to industry newsletters and maintain regular contact with compliance advisors, adjusting your operational policies as necessary to align with new regulations.

Recommended

Comments